Superannuation Tax Changes 2026: Australia’s superannuation system is entering a new phase in 2026, and the changes could reshape how retirees manage their wealth. If you’ve built a large super balance—or plan to—these updates are worth your attention. The introduction of a new tax rule is shifting the focus from generous concessions to a more targeted approach.

What’s Changing in Superannuation Tax 2026?

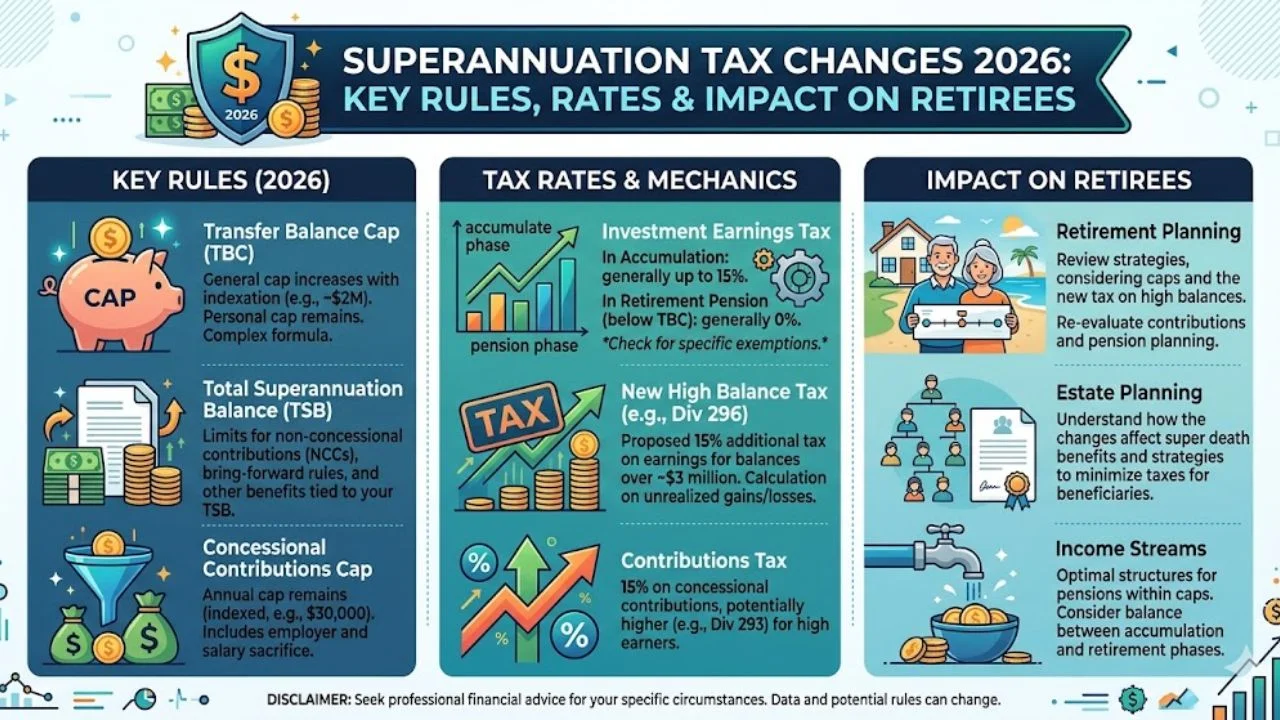

From July 1, 2026, the government is introducing a new tax framework aimed at high-balance super accounts. The goal is simple: keep super as a retirement tool, not a tax shelter for very large wealth.

Key update:

- New Division 296 tax applies to balances above $3 million

- Additional tax on earnings, not total balance

- Higher thresholds for extremely large accounts

Understanding the Division 296 Tax

The biggest change is the introduction of Division 296 tax.

How it works:

- Standard tax on super earnings: 15%

- Additional 15% tax on earnings above $3 million

- Extra 10% tax for balances above $10 million

Example:

If your super balance is $4 million, only the earnings from the extra $1 million are taxed at the higher rate.

Key takeaway:

This is a targeted tax—not a blanket increase.

Super Contribution Limits and Rates (2026)

Understanding contribution caps is essential for smart planning.

Updated limits:

| Metric | 2025–2026 | 2026–2027 (Estimated) |

|---|---|---|

| Super Guarantee (SG) | 12% | 12% |

| Concessional Cap | $30,000 | $32,500 |

| Non-Concessional Cap | $120,000 | $130,000 |

| Transfer Balance Cap | $2,000,000 | $2,100,000 |

| Division 296 Threshold | N/A | $3,000,000 |

Why it matters:

These caps help you control how much you contribute and avoid unnecessary tax exposure.

Impact on Retirees and High-Balance Investors

The new rules mainly affect individuals with super balances above $3 million.

What changes for you:

- Only earnings above the threshold are taxed more

- Existing balances are not fully taxed

- Investment income like dividends and interest is included

Important relief:

Unrealized gains (like property value increases) are not taxed until realized.

Smart Strategies Before July 2026

Planning ahead can help reduce your tax burden.

Practical strategies:

- Consider contribution splitting with your spouse

- Monitor your total super balance across accounts

- Adjust investment structures if needed

- Seek professional financial advice

Cost Base Reset Explained

One of the most important opportunities is the cost base reset.

What it means:

- You can reset asset values to market value as of June 30, 2026

- Only future gains will be taxed under new rules

Why it’s useful:

It protects past investment growth from additional taxation.

Long-Term Impact on Australia’s Retirement System

These reforms are designed to make the system more sustainable. While only a small percentage of Australians will be directly affected, the changes signal a shift toward fairness and long-term stability.

For most workers, higher contribution caps and steady SG rates will continue to support retirement savings growth.

Key Takeaways

- New tax applies only to super balances above $3 million

- Earnings—not total balance—are taxed at higher rates

- Contribution caps are increasing gradually

- Cost base reset offers a valuable planning opportunity

- Early financial planning is essential

FAQs

1. Does the new tax apply to my entire super balance?

No, it only applies to earnings on the portion above $3 million.

2. What is the cost base reset option?

It allows you to reset asset values to June 30, 2026, so only future gains are taxed.

3. Will the $3 million threshold change?

Yes, it is expected to increase over time with inflation.

4. Who is most affected by these changes?

High-balance individuals and retirees with more than $3 million in super.

5. Should I change my investment strategy now?

It depends on your balance and goals—professional advice is recommended.

Conclusion

The 2026 superannuation tax changes mark a significant shift in Australia’s retirement landscape. While most Australians won’t be directly affected, those with larger balances need to rethink their strategies. With the right planning, it’s still possible to grow your retirement savings efficiently while staying within the new rules. The key is to act early, stay informed, and make smart financial decisions.